Clik here to view.

Despite working hard all their lives to save for their golden years, many retirees — even affluent retirees — tend to underspend after they’ve retired. Research shows that few are systematically drawing down their savings. This period of planned spending of assets acquired to fund retirement is known as decumulation. The fact that most retirees don’t spend as much as they safely could – or spend as much as many retirement strategies assume – is the “decumulation paradox.”

Clik here to view.

“The decumulation paradox, fundamentally, is the misalignment between assumed behavior of retirees once they reach retirement … and what’s observed,” said Todd Taylor, senior vice president and head of annuities for New York Life. Taylor, along with Kelli Faust, corporate vice president and actuary at New York Life, authored “Understanding underspending in retirement: The Decumulation Paradox reexamined.”

“Many people have saved all their lives with the idea of living comfortably in retirement,” explained Taylor. “In practice, we observed that many folks are actually not spending down their assets and [are] continuing to hold on to assets in retirement. Hence, this paradox.

“A few years ago, we stumbled onto this. We had done a survey of American consumers — most of whom are generally affluent retirees — and we wanted to ask them essentially if they knew what a safe withdrawal rate was. Our intent was to demonstrate that despite all this research around the 4% rule, many people didn’t know what a safe withdrawal rate was. They gave us all kinds of crazy answers, like 30 … 8 … 52.”

An 'aha moment'

Beyond showing that many retirees didn’t know the traditionally accepted annual spending rule of 4%, the research produced a real “aha moment,” said Taylor.

Many weren’t spending down their assets at all, he said, adding, “We’ve subsequently done more research. And that led to this whole body of work that we wrote about.”

Nobel Prize-winning professor of finance William F. Sharpe once called running out of money in retirement “the nastiest, hardest problem in finance,” said Taylor. “Now, if you’re a Nobel laureate and you can’t figure this out, imagine if you’re an everyday investor,” he said.

A conservative spending approach

In the face of complexity in today’s environment with all the uncertainties of the market, said Taylor, many have taken a conservative approach of “Let me hold on to what I have, let me spend at a much lower rate.” This is “a form of self-insuring your own retirement,” he said, adding that by taking this approach, retirees are “avoiding all that complexity.”

Taylor has studied and written about retirement for the better part of the past 10 or 15 years; much of his work was based on modeling spend-down strategies. He says that a few years ago he had an interesting discussion with his then 93-year-old grandmother, who had been living in retirement for 35 or 40 years. He asked her, “What’s your spend-down strategy … what’s your retirement strategy?”

“She essentially said some version of ‘I don’t spend down. We figure out how much money comes in every month, and then I spend a little bit less than that, and I guarantee that I won’t run out of money that way.’”

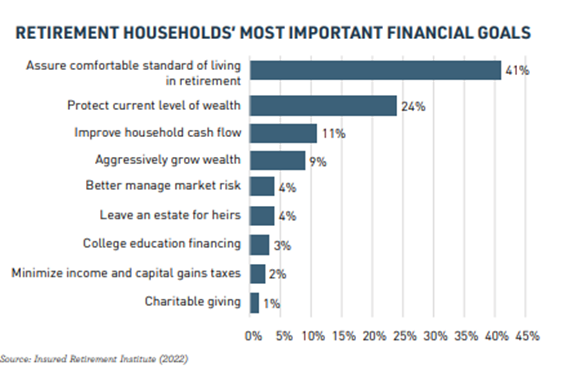

Taylor said that when she passed, she ended up leaving a bequest to the family. “Now, this was modest, it wasn’t any significant windfall, but it effectively was money that we didn’t need and she didn’t really want to give to us. What she really wanted to do was to enjoy her retirement for those prior 35 years. And this isn’t just my grandmother. There’s consistent research on this. Very consistently, if you ask retirees ‘What are your top goals?’ No. 1 is ‘live comfortably in retirement.’ And just about the last one is something along the lines of ‘leave a bequest or leave money to my heirs.’ ”

Image may be NSFW.

Clik here to view.

“By underspending,” Taylor explained, “effectively what people are doing is leaving money to their heirs, which, to put it in economic terms, is not maximizing utility. They want to spend money. And so that’s really the problem and somewhat of a paradox as well.

“You hold on to assets in the event that you need a new roof or you end up in a nursing home or you have some kind of major medical expense or whatever.

Image may be NSFW.

Clik here to view.

“What’s interesting about that is in all the other aspects of our lives, especially before you retire, we have a good solution for that. And it’s insurance. It’s the fundamental purpose of insurance. I have two little kids. We moved to the suburbs about a year and a half ago, and we bought homeowners insurance because we wanted to ensure the value of our home. Now, I’m not trying to win against my property and casualty insurer and get a good return on that. In fact, I obviously don’t want to do that. I don’t want to hold the entire value of my house in cash in case it burns down. That’s really, really inefficient. So that low-probability event is protected very nicely by my homeowners insurance.”

With regard to this self-insuring behavior, the research revealed the behavioral differences of the people who had “some form of guarantee associated with the retirement,” said Taylor.

“The greatest example of this is having a defined benefit pension," he said, adding, "Vanguard did this study a few years ago, which we mentioned in our paper. They basically broke people into categories according to the sources of their income in retirement.” In addition to what the source of retirement income was, Vanguard controlled for other factors, such as overall wealth, age, etc.

“What they found,” said Taylor, “was that those who had pensions, holding everything else equal, spent more in retirement. And, interestingly, we found this held in a bunch of other examples. EBRI did this study showing that … those who had long-term care insurance, again holding all else equal, spent something like 30% or 50% more in retirement.”

The value of peace of mind

“It’s just the presence of the insurance,” he said, adding, “It’s that peace-of-mind value.

“And obviously interesting to us as well was the value of having an annuity in your portfolio. We found this data set from the University of Michigan that showed the same thing. If you held an annuity, you actually spent more. The self-insurance appears to be an aspect of why people are holding on to their assets. They’re holding on to them to protect against some event. But in any other walk of life, we’d insure for those things - those low-probability, high-impact events - and basically be able to better enjoy yourself in the meantime.

“There is a well-documented phenomenon that a number of folks have referred to as the ‘spending smile.’ It’s the idea that if you look at nominal spending in retirement, it starts highest and then it begins to decline over time with sort of your inability to travel, to move around, to take that vacation, etc. And then it ticks up back at the end as a result of perhaps late-in-life health costs, etc. So, there is sort of a natural pattern to spending, which, by the way, also is at odds with the 4% rule, which basically says you take the same amount and adjust it for inflation every year.”

Taylor said that this spending smile is “another example of perhaps our models for figuring out optimal strategies being disconnected from how people are actually behaving.”

The New York Life researchers looked at four different types of behavior that they theorize may be leading retirees to hold back on spending in retirement.

Loss aversion

“Many of these behavioral biases are in some ways speculation on what is driving some of this paradoxical behavior,” said Taylor. “Loss aversion is basically the idea that you’re thinking more about the bad outcomes that might happen. Now there’s a whole mountain of research on behavioral economics. There are luminaries in this area who have demonstrated that people exhibit this behavior.”

Essentially, explained Taylor, “People dislike losses more than they like gains. And if you apply that to retirement, there’s been research that’s demonstrated that loss aversion is even more material in retirement. Basically, once you’ve saved and you don’t have an additional sort of labor income coming in, you’re so anchored to holding on to that principle you’ve saved that it makes you very, very averse to seeing the balance drop.”

Familiarity bias

“As you save all the way through retirement, your basic rule is to make sure you don’t spend more than you bring in. If you do that, your retirement nest egg — all else being equal — will grow. Retirement is a big step. It’s difficult, I think, for folks to go from saving for the last 30 or 40 years to, all of a sudden, doing the opposite. And the familiarity bias is again following that simple rule of 'don’t spend more than you bring in' because you’ve been doing that for the last 35 years.”

Mental accounting

“Mental accounting is basically the idea of putting things into buckets. If there was a steady stream of income coming in, people would spend it. You can think of two different stocks or two different mutual funds: one that generates dividends, one that gets its returns through capital gains. The mental accounting is saying that if I get this recurring dividend over time, I feel comfortable spending that.” Taylor explained that people who own stocks and received dividends would spend those to a greater degree than would those who had a greater percentage of their stock earnings coming through capital gains. “Economically, it makes no sense, but it’s this mental accounting,” he said.

“We talk a little bit about some of the opportunities that advisors have to try to get their clients to actually spend more when they safely can. And one strategy may actually be tilting folks into stocks that provide dividends or interest-bearing accounts that give people this idea that they’re getting this steady stream of income, even though, of course, dividends are not guaranteed for any length of time.”

The endowment effect

“I might lump the endowment effect in with the behavioral concept of anchoring. It’s basically the idea that once you’ve achieved a certain level of wealth, it becomes very important to you to hold on to that. And you actually do see that in the data as well. So, we mentioned most retirees say their No. 1 goal is to live comfortably in retirement. Leaving a bequest shows up just basically dead last. But something else that scores relatively well is this concept of ‘preserving my level of wealth.’

“Now, of course, that’s pretty at odds with the first goal, which is problematic. If you want to spend more, you may see your level of wealth go down.” Taylor said the level of savings that’s been achieved prior to retirement is “a number you can sort of fixate on. It’s something that you feel good about, and I think that’s leading to some of this behavior, this idea of preserving a certain level of wealth.”

How can an advisor help?

“The point of our paper was probably two things. First, we need to develop plans for consumers based on how they actually live and how they actually behave, not how we assume they’re going to live.

“The assumption that many models make that people buy and hold is just plain not correct. People don’t buy and hold. We should just stop assuming that. We should start assuming that people actually do buy and sell stocks. No matter how many academics say it’s a bad idea, they do it.

“Let’s not start every retirement planning conversation assuming people are going to spend at 4% and increase it by inflation year after year after year. We need to design plans based on how people are going to behave, and we need to talk to our clients and consumers about how they actually intend to behave in retirement."

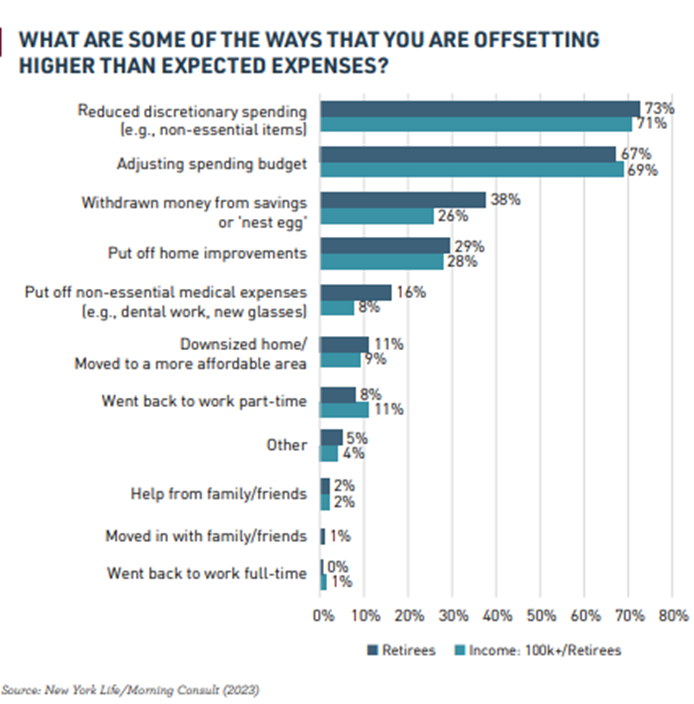

The New York Life study found that retirees are more likely to reduce discretionary spending (73%) or adjust their budgets (67%) than to draw down from their savings or a nest egg.

“Second, it’s this idea that the value of guarantees in the person’s portfolio is peace of mind. They know that they can live to 110 and the insurance company is going to pay them off. And so what that means is peace of mind, which to me, five years ago, felt very fluffy. I’m a quantitative guy by background. Peace of mind is kind of amorphous. But this research shows that peace of mind actually does something. It actually changes people’s behavior.”

Taylor said he believes the lesson for advisors is that if folks are exhibiting behavior that implies that they’re self-insuring against risks, advisors should help them evaluate whether it makes more sense to actually insure that risk or to bear the cost of that self-insurance, which in many cases is essentially underspending.

“It’s really a question of how people are actually behaving and adjusting plans for that,” said Taylor. “And then looking at the value of guarantees, which, in many cases, can actually change a retiree’s behavior in positive ways.”

Editor's Note: Find the full version of "Understanding Underspending in Retirement: The Decumulation Paradox Reexamined" here.

John Forcucci is InsuranceNewsNet editor-in-chief. He has had a long career in daily and weekly journalism. Contact him at John.Forcucci@innfeedback.com. Follow him on Twitter @INNJohnF.

© Entire contents copyright 2024 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

The post The Decumulation Paradox: Why many retirees underspend appeared first on Insurance News | InsuranceNewsNet.